Managerial Accounting For Dummies by Mark P. Holtzman

Author:Mark P. Holtzman

Language: eng

Format: epub

Publisher: Wiley

Published: 2013-01-17T16:00:00+00:00

Illustration by Wiley, Composition Services Graphics

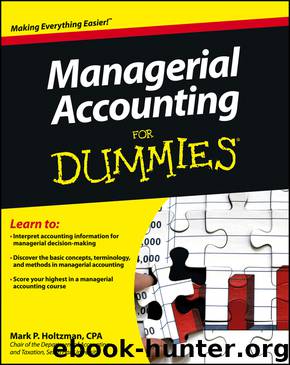

Figure 9-7: Graphing margin of safety.

Making use of formulas

To compute margin of safety directly, without drawing pictures, first calculate the break-even point and then subtract it from actual or projected sales. You can use dollars or units:

For guidance on finding the break-even point, check out the earlier section Generating a Break-Even Analysis.

You can compute margin of safety either in sales dollars or in units, but be consistent. Don’t subtract break-even sales in units from actual sales in dollars!

Taking Advantage of Operating Leverage

Operating leverage measures how changes in sales can affect net income. For a company with high operating leverage, a relatively small increase in sales can have a fairly significant impact on net income. Likewise, a relatively small decrease in sales for that same company will have a devastating effect on earnings.

Operating leverage is typically driven by a company’s blend of fixed and variable costs. The larger the proportion of fixed costs to variable costs, the greater the operating leverage. For example, airlines are notorious for their high fixed costs. Airlines’ highest costs are typically depreciation, jet fuel, and labor — all costs that are fixed with respect to the number of passengers on each flight. Their most significant variable cost is probably just the cost of the airline food, which, judging from some recent flights I’ve been on, couldn’t possibly be very much. Therefore, airlines have ridiculously high operating leverage and unspeakably low variable costs. A small drop in the number of passenger-miles can have a dreadful effect on an airline’s profitability.

Graphing operating leverage

In a cost-volume-profit graph (see Figure 9-3 earlier in the chapter), operating leverage corresponds to the slope of the total costs line. The more horizontal the slope of this line, the greater the operating leverage. Figure 9-8 compares the operating leverage for two different entities, Safe Co., which has lower operating leverage, and Risky Co., which has higher operating leverage.

Download

This site does not store any files on its server. We only index and link to content provided by other sites. Please contact the content providers to delete copyright contents if any and email us, we'll remove relevant links or contents immediately.

Zero to IPO: Over $1 Trillion of Actionable Advice from the World's Most Successful Entrepreneurs by Frederic Kerrest(4572)

Machine Learning at Scale with H2O by Gregory Keys | David Whiting(4313)

Never by Ken Follett(3957)

Harry Potter and the Goblet Of Fire by J.K. Rowling(3858)

Ogilvy on Advertising by David Ogilvy(3622)

Shadow of Night by Deborah Harkness(3368)

The Man Who Died Twice by Richard Osman(3080)

Book of Life by Deborah Harkness(2939)

The Tipping Point by Malcolm Gladwell(2925)

Will by Will Smith(2920)

Purple Hibiscus by Chimamanda Ngozi Adichie(2855)

0041152001443424520 .pdf by Unknown(2846)

My Brilliant Friend by Elena Ferrante(2831)

How Proust Can Change Your Life by Alain De Botton(2814)

How to Pay Zero Taxes, 2018 by Jeff A. Schnepper(2655)

Hooked: A Dark, Contemporary Romance (Never After Series) by Emily McIntire(2555)

Rationality by Steven Pinker(2366)

Can't Hurt Me: Master Your Mind and Defy the Odds - Clean Edition by David Goggins(2341)

Borders by unknow(2315)